Aave, one of the leading lending protocols in DeFi (decentralized finance, which lets you lend and borrow crypto without banks), is gearing up for a major upgrade with V4. This update promises to be a big deal in 2025, introducing smarter ways to handle liquidity, borrowing, and risks. Based on insights from a recent thread by Pink Brains, let's break down what makes Aave V4 stand out and how it improves on the current V3.

Why Aave V4 Matters in DeFi

In the world of blockchain, DeFi protocols like Aave allow anyone to supply assets as collateral and borrow others, earning interest or leveraging positions. But V3 has some limitations, like fragmented liquidity across different markets. This means some pools sit idle while others are stretched thin, and risk settings treat all users the same, no matter their collateral quality.

Aave V4 tackles these head-on with a fresh approach. It's designed to make the protocol more efficient, secure, and user-friendly, attracting both everyday crypto enthusiasts and big institutions.

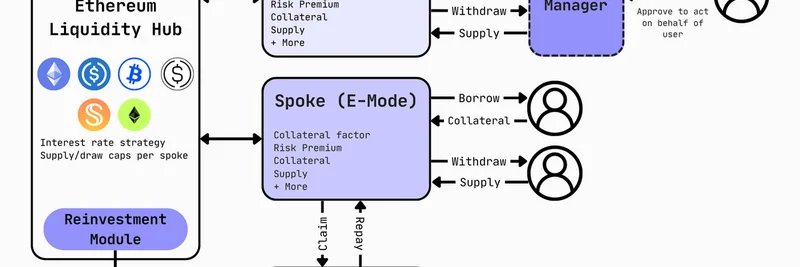

Unified Liquidity: The Hub-and-Spoke Model

At the heart of V4 is the Hub-and-Spoke architecture. Think of the Hub as a central liquidity pool on each blockchain, where all supply and demand converge. Spokes are like specialized modules—such as E-Mode for efficiency, real-world assets (RWAs), or custom vaults—that connect to this Hub but maintain their own risk isolation.

This setup ends the fragmentation in V3. Multiple markets can now pull from the same deep liquidity source, boosting efficiency. For example, if you're supplying ETH or BTC, it flows into the Hub, ready for borrowing across connected Spokes without silos.

Risk-Priced Borrowing for Fairer Rates

Borrowing in V4 gets smarter with Risk Premiums. Instead of a one-size-fits-all interest rate, your cost depends on your collateral's risk level. Blue-chip assets like ETH or BTC get the base rate, while riskier "long-tail" tokens add a premium. This means safer borrowers pay less, and lenders get better compensated for higher risks.

It's a win-win: encourages quality collateral and aligns incentives across the ecosystem.

Dynamic Risk Management

V3's risk updates could hit all users at once, sometimes triggering unexpected liquidations (when your position is force-sold to cover debts). V4 fixes this by assigning a "risk ID" to each update. Existing positions stick to their original settings, while new ones adopt the latest. You only switch if you increase risk, making everything more predictable and safer.

Upgraded Liquidation Engine

Liquidations are crucial in DeFi to protect lenders, but they can be harsh. V4's new engine lets liquidators repay just enough debt to restore a position's health factor (a measure of how safe your loan is), rather than taking a fixed chunk. Bonuses scale with risk, incentivizing quick action.

This should make liquidations faster, fairer, and less punitive for borrowers.

Reinvestment Module for Idle Capital

Unused liquidity in the Hub can now be optionally reinvested into external yield strategies, all governed by the community. This turns idle funds into extra earnings, potentially boosting overall returns for suppliers.

Additional Features and Future Plans

V4 isn't stopping at launch. It includes gas-saving multicall transactions (batching actions), position managers for acting on behalf of users, and UX tweaks. Post-launch, expect permissionless Hubs for devs, auto-adjusting borrow curves, smart accounts for isolated collateral, advanced oracles, treasury tools, and enhancements to Aave's stablecoin GHO (like deeper minting and soft liquidations).

The roadmap points to a public testnet soon, with mainnet in Q4 2025.

Aave V4 could redefine DeFi lending, making it more accessible and robust. Whether you're into meme tokens or serious crypto strategies, keeping an eye on protocols like Aave helps you navigate the blockchain world smarter. For more updates, check out Aave's official site or follow discussions on X.