Ever feel like the world of decentralized finance (DeFi) is moving at warp speed? If you're knee-deep in blockchain or just dipping your toes into meme tokens and crypto lending, you've probably noticed the buzz around lending protocols. They're not just surviving—they're thriving, hitting new all-time highs month after month. According to a recent thread from Blockchain Bureau, the total outstanding debt in DeFi lending now sits at a whopping $30.4 billion. That's a mind-blowing 711% jump from two years ago. And the star of the show? Stablecoin credit, which seems to have an insatiable appetite among borrowers.

For the uninitiated, DeFi lending lets you borrow or lend cryptocurrencies directly on the blockchain, cutting out the middleman like traditional banks. Platforms like Aave, Compound, and Venus make it possible, often with stablecoins (think USDC or USDT, which hold steady value pegged to the dollar) as the go-to for loans. This surge signals growing confidence in DeFi's infrastructure, but it also highlights some fascinating differences across protocols.

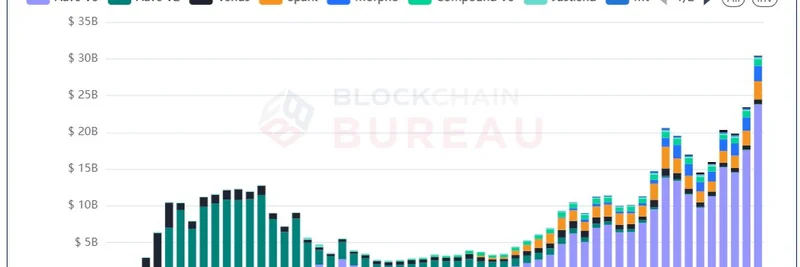

Take a look at this chart—it's a visual feast of growth. Aave V3 (that purple bar climbing high) dominates, but you've got Venus, Spark, Morpho, Compound V3, JustLend, and others stacking up impressive volumes. From humble beginnings in late 2020, the total debt has skyrocketed, especially post-2022. It's a testament to how DeFi has matured, turning what was once a niche experiment into a multi-billion-dollar ecosystem.

But not all protocols are created equal when it comes to risk and performance. Blockchain Bureau points out that liquidation rates (that's when loans get automatically sold off if collateral drops too low) and repayment track records vary wildly. This directly impacts each platform's "creditworthiness"—essentially, how reliable it is for lenders and borrowers. Curious about the nitty-gritty? Their dashboard breaks it down with real-time data, perfect for blockchain practitioners sharpening their edge.

Here's where it gets interesting: credit scores per protocol tell a story of diversity. In this distribution chart, you see Aave V3 and Compound V3 skewing toward higher scores (around 600-650, where most users cluster), while others like Silo V2 spread a bit wider. Higher scores mean better repayment behavior overall, which could explain why some platforms attract more volume. If you're building strategies around meme tokens or yield farming, picking a protocol with solid credit metrics isn't just smart—it's essential.

Shifting gears to costs, borrow rates have flipped the script since October 2023. Stablecoin rates have pulled ahead of non-stable ones, driven purely by demand. Right now, the average stablecoin borrow rate hovers at 8%, compared to just 3.1% for volatile assets like ETH or BTC. It's a clear sign that folks want that rock-solid borrowing power for leveraged plays, perhaps in trading meme coin pumps or hedging positions.

This rate divergence isn't random—it's demand pulling stablecoin lending into overdrive. As Blockchain Bureau notes in their thread, it's a flip from earlier trends where non-stables ruled. For meme token enthusiasts, this could mean cheaper leverage on wild rides if you stick to stables, but watch those liquidations!

Wrapping it up, this DeFi lending boom isn't just numbers on a chart—it's a pulse check on blockchain's evolution. With $30B+ in play and stablecoins leading, opportunities abound for savvy users. Head over to Blockchain Bureau's dashboards to track it live, and keep an eye on how it ripples into meme token liquidity. What's your take—bullish on lending, or waiting for the next twist? Drop your thoughts below.