Hey folks, if you've been keeping an eye on the wild world of decentralized finance (DeFi), you know it's been evolving faster than a meme coin during a bull run. But lately, things are getting really interesting with what's being called "Programmable Finance." I came across this insightful thread from ANAGRAM, a crew that's all about modern takes on blockchain tech, and it highlights just how massive onchain lending has become. We're talking protocols holding over $100 billion in liquidity and managing a whopping $42 billion in active loans. Yeah, you read that right—onchain banks are now rivaling the big traditional players.

Let's break it down simply. DeFi started as a

- Let's consider how to tie DeFi trends to meme tokens for relevance.

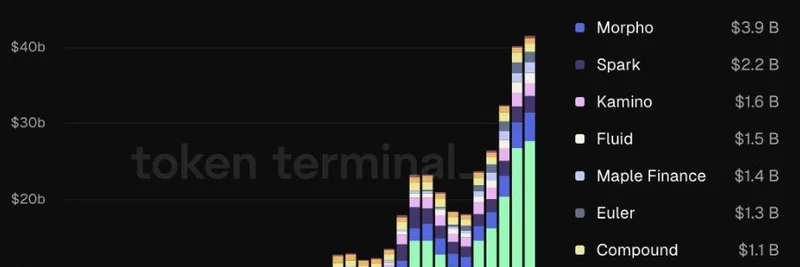

way to lend, borrow, and trade crypto without middlemen, but now it's leveling up to "programmable" stuff. That means money isn't just sitting there; it's smart, automated, and works across different apps seamlessly. The thread points to data from Token Terminal, showing this growth in a killer chart.

Look at that graph—it's a stacked bar chart tracking active loans monthly over the past three years. You can see the explosion starting around mid-2023, with protocols like Aave (in green) dominating at $28.1 billion latest, followed by Morpho ($3.9B), Spark ($2.2B), and others like Kamino, Fluid Finance, Maple Finance, Euler, Compound, Venus, and Moonwell. There are even 12 more projects not shown, but get this: nine protocols alone have over $2 billion in deposits each. It's like the crypto version of Wall Street, but open to anyone with an internet connection.

What makes this different from your average bank? For starters, you can lend or borrow pretty much any asset out there—stablecoins, ETH, even niche tokens. Yields kick in instantly, no waiting for interest to compound monthly. And the real magic? It's all programmable and composable. Imagine your loan terms auto-adjusting based on market conditions or integrating directly with other DeFi apps for seamless trades or payments. No more silos; it's all connected.

The thread ties this back to a bigger shift from basic DeFi (think yield farming and speculation) to something more practical. ANAGRAM's full blog post dives deeper, mentioning how giants like BlackRock are holding $80B in Bitcoin ETFs, MicroStrategy with $70B+ in BTC, and Aave sitting on $66B in deposits—bigger than some legacy banks like Barclays or Deutsche Bank. Human and financial capital is flooding onchain, and now the focus is on making it usable for real life.

One exciting part is bridging this to everyday spending. Projects like Ether.fi, KAST Card, Payy, and Privy are rolling out Visa cards backed by onchain deposits, Apple Pay with stablecoins, even tap-to-pay crypto. Stake your assets, earn yield, and spend it at the coffee shop—all without leaving the blockchain. Wallets are getting smarter too, with built-in privacy tech like zero-knowledge proofs (ZK), multi-party computation (MPC), and fully homomorphic encryption (FHE) to keep things secure and private.

And don't get me started on programmable identity. Smart wallets could handle KYC and AML checks in a privacy-preserving way, using tools from projects like Fairblock or zkTLS. This combo of compliance and confidentiality? It's key to bringing in the masses without sacrificing decentralization.

In the end, as the thread wraps up, DeFi 1.0 was all about speculative yields, but DeFi 2.0—or Programmable Finance—is about real utility. Money that works for you: paying bills in stables, auto-earning yield, and tying into self-sovereign identity. No intermediaries, no censorship—just pure, onchain efficiency.

If you're a blockchain practitioner or just dipping your toes into crypto, this is the kind of evolution that could make meme tokens and beyond way more integrated into daily finance. Keep an eye on these lending protocols; they're not just numbers on a chart—they're building the future of money. What do you think—ready to lend your crypto and spend the yields IRL? Drop your thoughts below!