Sam Bankman-Fried, the disgraced founder of FTX, recently shared a document detailing what he claims happened to the billions of dollars lost in the exchange's 2022 collapse. Posted from his account managed by a friend while he's serving time, the thread sparked reactions across the crypto community, including a pointed response from Patrick Collins, co-founder of Cyfrin Audits and a prominent figure in Web3 security.

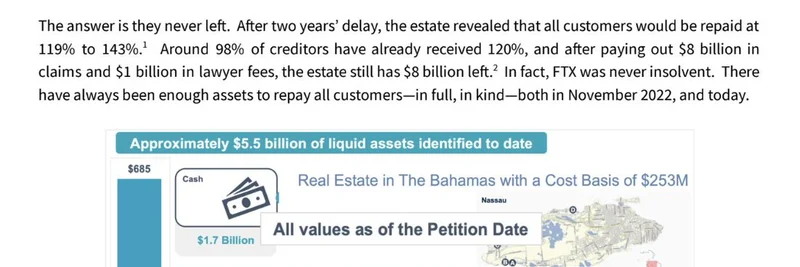

In the document titled "FTX: Where Did the Money Go?", SBF argues that FTX wasn't actually insolvent but faced a temporary liquidity crunch. He points out that customer deposits totaled around $20 billion, but when a run on the exchange hit in November 2022, FTX filed for bankruptcy owing $8 billion. Fast forward to now, and the estate is repaying creditors at 119% to 143% of their claims, with 98% already receiving 120%. SBF emphasizes that assets like investments in Anthropic, Solana tokens, and other ventures have appreciated massively, turning what could have been losses into gains.

He breaks it down: FTX always had enough assets to cover liabilities, including illiquid holdings that ballooned in value post-crash. For example, their 58 million Solana tokens, bought cheap, are now worth billions amid Solana's resurgence—home to many popular meme coins today. SBF blames external lawyers for seizing control, delaying repayments, and "dollarizing" claims (converting crypto values to USD at bankruptcy filing prices), which shortchanged users as prices soared.

But not everyone's buying it. Patrick Collins quote-tweeted SBF's post with a meme from a movie scene saying "Don't believe his lies," and a scathing analogy: “I didn’t lose your money, I bet your money all on black, but it came up red. But the most recent roulette spin came up black, which proves that I was correct to take your money without your consent and bet your money all on black.”

Collins' point hits hard in the crypto world, where trust is everything. SBF's narrative frames his risky bets as vindicated by market recoveries, but critics like Collins see it as unauthorized gambling with user funds—a cardinal sin in decentralized finance. This echoes broader concerns in the meme token space, where volatility is king, but exchanges are supposed to safeguard assets, not wager them.

Replies to Collins' tweet echo the sentiment. One user compared it to "classic gambler’s logic," while another noted how prediction markets (like those on Polymarket, a hot topic in crypto) blur lines with casinos. Even in defenses of SBF, like one reply suggesting the money would've returned without liquidation, Collins pushed back: it wasn't SBF's to risk in the first place.

This dust-up reminds blockchain practitioners why audits and transparency matter. As meme tokens on chains like Solana explode—think Dogwifhat or Bonk—understanding past failures like FTX helps avoid repeats. If you're diving into meme investing, tools like Cyfrin Audits or CodeHawks can help vet projects.

SBF's full doc is available here, but take it with a grain of salt. In crypto, hindsight's 20/20, but consent and custody are non-negotiable. What's your take—vindicated visionary or reckless gambler?